The infrastructure layer · The cloud race · The model makers · The hidden winners · What it means for your strategy

Last Updated: February 2026 | Related: 140+ AI Statistics Every Business Leader Must Know →

A Reddit commenter said it plainly: "Only person making money in this scam is Nvidia."

52 people upvoted that. Not because it's entirely accurate — but because it captures something real. While headlines celebrate AI adoption milestones, a quieter question sits underneath all of it: who is actually capturing the economic value being created?

We already established in our AI statistics roundup that 88% of companies have adopted AI, but only 6% are seeing meaningful ROI. That gap — between investment and return — is the central mystery of the AI era.

To understand it, you have to follow the money upstream.

Here is where it is actually going.

The Gold Rush Analogy Most People Misread

During the California Gold Rush, the people who reliably got rich were not the prospectors. They were the merchants selling shovels, picks, denim trousers, and food. The prospectors mostly broke even or lost money.

The people selling the tools to the diggers built lasting fortunes.

AI is following the same structure. The organizations investing in AI — the 88% — are the prospectors. The companies selling the infrastructure to run AI are the shovel merchants. And right now, the shovel merchants are winning by a margin that is almost impossible to overstate.

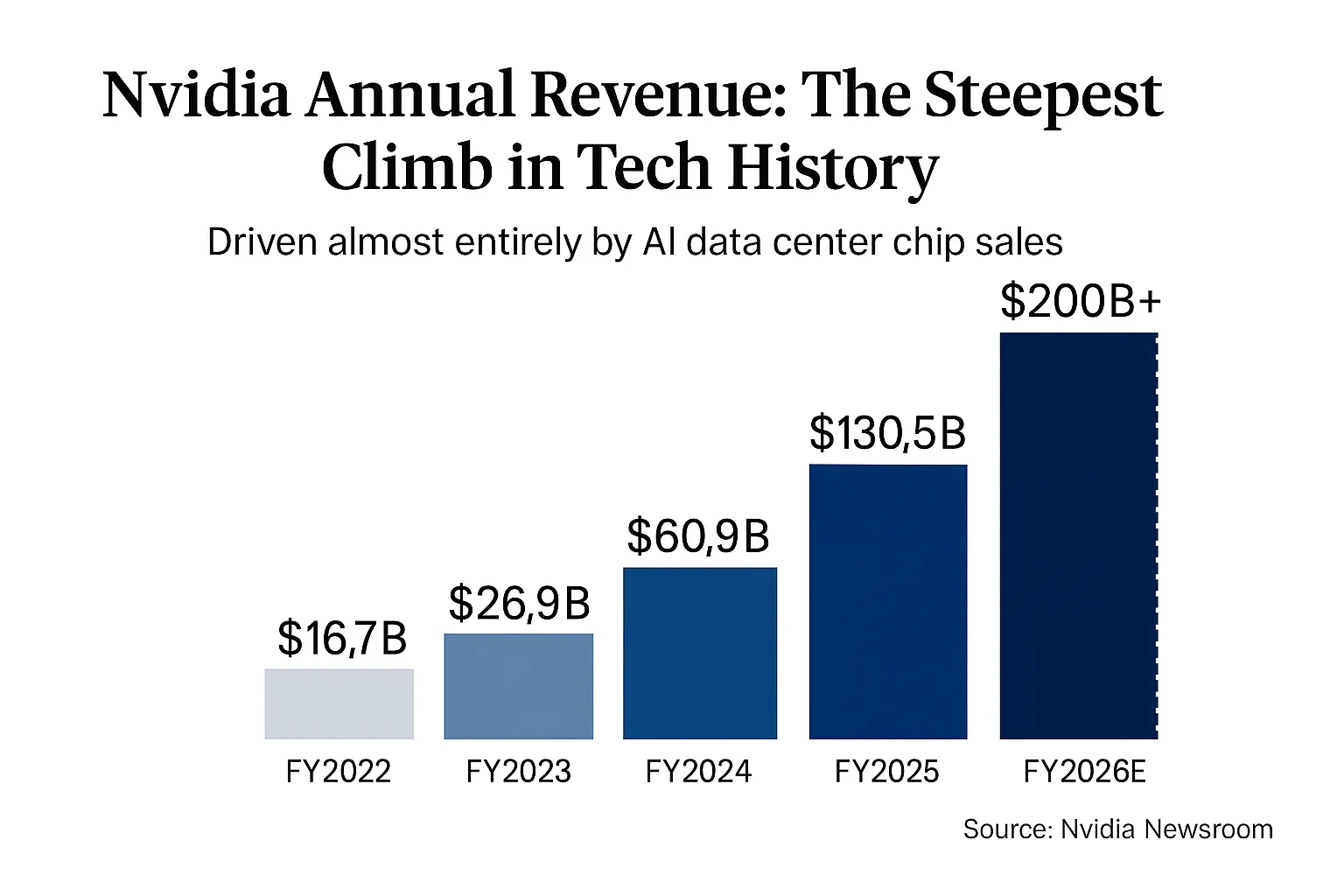

1. Nvidia: The Numbers Are Not Normal

Let's start with the data, because the scale of what is happening at Nvidia defies casual description.

Statistic | Data Point | Source |

|---|---|---|

Nvidia full-year revenue, fiscal 2025 (ended Jan 2025) | $130.5 billion (+114% year-over-year) | |

Nvidia data center revenue, fiscal 2025 | $115.2 billion (+142% year-over-year) | |

Nvidia Q3 FY2026 quarterly revenue (Oct 2025) | $57 billion (+62% year-over-year) | |

Nvidia Q3 FY2026 data center revenue alone | $51.2 billion (+66% year-over-year) | |

Nvidia gross margin (Q3 FY2026) | 73.6% | |

Nvidia Q4 FY2026 revenue guidance (Jan 2026) | $65 billion (guided; results due Feb 25, 2026) | |

Nvidia FY2024 EPS growth | +586% year-over-year | |

Nvidia AI infrastructure market estimate (Huang, end of decade) | $3–4 trillion annually | |

Nvidia peak market valuation (July 2025) | $4 trillion — first company in history |

A 73.6% gross margin means Nvidia keeps nearly 74 cents of every dollar it earns from data center sales before operating expenses. For context: Apple, one of the most profitable consumer companies in history, runs gross margins around 44%. Nvidia's margins are not just high — they reflect a near-monopoly on the chips that every AI system in the world currently depends on.

A 73.6% gross margin means Nvidia keeps nearly 74 cents of every dollar it earns from data center sales before operating expenses. For context: Apple, one of the most profitable consumer companies in history, runs gross margins around 44%. Nvidia's margins are not just high — they reflect a near-monopoly on the chips that every AI system in the world currently depends on.

On the Q3 FY2026 earnings call, Jensen Huang described the state of demand simply: "The clouds are sold out and our GPU installed base, both new and previous generations, is fully utilized."

Q4 FY2026 results — which will cover the quarter ending January 25, 2026 — are due February 25, 2026. Analysts are projecting another record quarter.

⚡ Key Takeaway: Nvidia's data center revenue grew 142% in a single fiscal year and is on track to exceed $200 billion annualized in fiscal 2026. No company its size has ever grown this fast. The shovel merchant is not just winning — it is lapping the field.

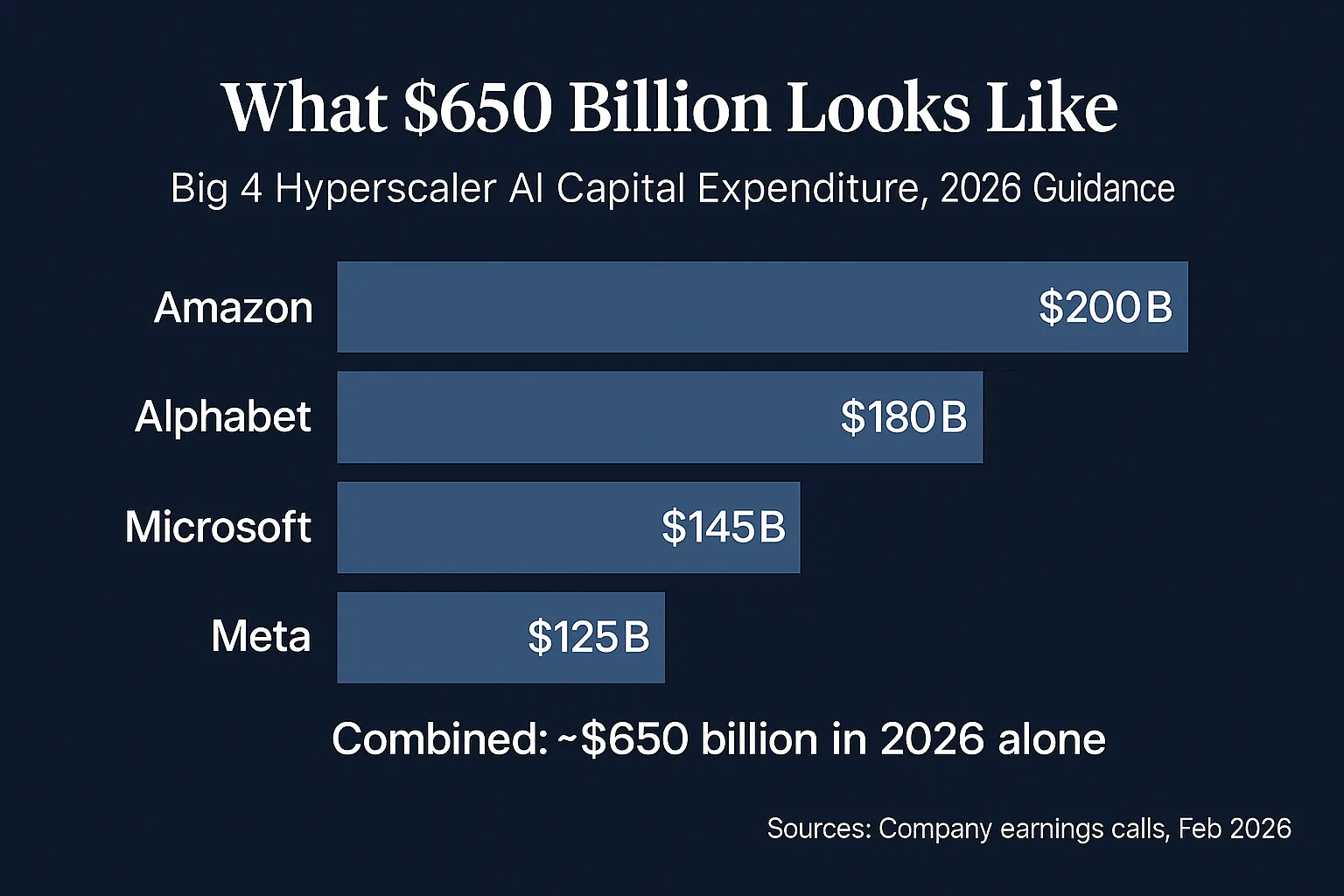

2. The Hyperscalers: $650 Billion and Counting

The four hyperscalers — Amazon (AWS), Microsoft (Azure), Google (Alphabet), and Meta — are engaged in what Fortune called "the largest capital investment in human history concentrated in a single purpose."

Statistic | Data Point | Source |

|---|---|---|

Big 4 combined capex, 2024 | ~$241 billion (+62% from 2023) | |

Big 4 combined capex, 2025 | ~$381 billion (+64% from 2024) | |

Big 4 combined capex, 2026 guidance | ~$650 billion (+70% from 2025) | |

Amazon 2026 capex commitment | $200 billion | |

Alphabet 2026 capex guidance | $175–$185 billion (+98% from 2025) | |

Meta 2026 capex guidance | $115–$135 billion | |

Microsoft 2026 capex (run rate based on H1 FY2026) | ~$140–$150 billion | |

Total Big 4 cash and equivalents on hand | $420 billion+ | |

Amazon projected free cash flow, 2026 | Negative $17–28 billion | |

Alphabet free cash flow projected drop, 2026 | ~90% decline to ~$8.2B from $73.3B in 2025 | |

Meta free cash flow projected drop, 2026 | ~90% decline | |

Combined Big 4 market cap loss after capex announcements | ~$950 billion |

The $650 billion number is not theoretical — it comes from binding capex commitments disclosed in earnings calls completed in January and February 2026. To put the scale in context: $650 billion rivals the annual GDP of Sweden. It is roughly triple what these four companies spent just two years ago.

The $650 billion number is not theoretical — it comes from binding capex commitments disclosed in earnings calls completed in January and February 2026. To put the scale in context: $650 billion rivals the annual GDP of Sweden. It is roughly triple what these four companies spent just two years ago.

Critically, Wall Street has consistently underestimated this spending: analysts forecast 19% growth in hyperscaler capex for 2024 — it came in at 54%. They forecast 22% for 2025 — it came in at 64%. The 2026 consensus estimate started at 19% growth. The actual guidance came in at 70%.

Who Is Actually Converting the Spend Into Revenue

Spending and earning are different things. Here is where the cloud revenue story diverges significantly between the four:

Provider | 2025 Cloud Revenue (est.) | YoY Growth | Revenue Backlog |

|---|---|---|---|

AWS | ~$127B | ~18% | Growing |

Microsoft Azure | ~$88B | ~33–39% | Doubled to $625B (OpenAI-driven) |

Google Cloud | ~$71B | ~32–48% | More than doubled in Q4 2025 |

Meta | No direct cloud revenue line | — | Internal AI only |

Sources: Campaign US, Feb 2026; Motley Fool, Feb 2026

Microsoft is targeting $25 billion in AI-specific revenue by end of fiscal 2026. Google Cloud revenue grew 48% year-over-year to $17.7 billion in Q4 2025 alone, with Gemini models as the primary driver.

Meta is the outlier. It has no direct cloud revenue line — every dollar of its $115–135 billion capex is an internal infrastructure bet tied to its own AI products and advertising efficiency. Analysts at Barclays project Meta's free cash flow will collapse by nearly 90% in 2026.

The unified concern across all four: analyst projections warn that free cash flow across the group could drop up to 90% in 2026 as capital expenditure outpaces AI revenue generation. The market reacted immediately — the four companies lost a combined ~$950 billion in market cap in the days following their capex announcements.

⚡ Key Takeaway: The hyperscalers are spending $650 billion in 2026 on a bet that AI compute is "the next winner-take-all market." AWS and Azure are the closest to justifying the spend with real revenue. Meta is the furthest, spending $115–135 billion with no direct AI revenue line to show for it. As TechCrunch put it: "Amazon and Google are winning the AI capex race — but what's the prize?"

3. The Model Makers: Revenue Is Real, Losses Are Larger

OpenAI ended 2025 with approximately $20 billion in annual revenue — a milestone that took Google seven years and Facebook six to reach. The problem is what it costs to generate it.

Statistic | Data Point | Source |

|---|---|---|

OpenAI annual revenue, end of 2025 | ~$20 billion | |

OpenAI projected operating losses, 2026 | ~$14 billion | |

OpenAI projected operating losses, 2028 | ~$74 billion | |

OpenAI cash burn rate, 2026–2027 | 57% of revenue | |

OpenAI cumulative negative cash flow, 2024–2029 (Deutsche Bank) | $143 billion | |

OpenAI total spending commitments (8-year) | $1.4 trillion | |

OpenAI projected profitable | 2029 (cash-flow positive) | |

OpenAI compute margin (Oct 2025) | 70% (up from 52% a year prior) | |

OpenAI ChatGPT web traffic share (Jan 2026) | 64.5% (down from 86.7% in Jan 2025) | |

Google Gemini web traffic share (Jan 2026) | 21.5% (up from 5.7% in Jan 2025) | |

Anthropic revenue ARR by August 2025 | $5 billion+ | |

Anthropic projected cash burn rate, 2027 | 9% of revenue (vs. OpenAI's 57%) |

The structural divergence between OpenAI and Anthropic is worth noting: both companies currently burn cash at similar rates relative to revenue, but their projected paths split sharply.

Anthropic is on track to reduce its burn rate to 9% of revenue by 2027. OpenAI projects its burn rate stays at 57% through 2026 and 2027 — a fundamentally different bet on scale over efficiency.

There is also a circular financing dynamic embedded in OpenAI's model. Nvidia committed up to $100 billion to OpenAI — money that, as OpenAI's CFO Sarah Friar acknowledged, will largely cycle back to Nvidia in GPU purchases. Nvidia is also a prominent investor in CoreWeave, which supplies cloud capacity to OpenAI and buys Nvidia chips to do so. The loop is visible once you look for it.

⚡ Key Takeaway: The model makers are not profit centers — they are the most expensive bets in corporate history. OpenAI will lose an estimated $14 billion in 2026 against $20–28 billion in revenue. The question is not whether they're losing money — it's whether the revenue trajectory is steep enough to eventually outrun the losses. Deutsche Bank estimates $143 billion in cumulative negative cash flow before that happens.

4. The Hidden Winners: Energy and Infrastructure

This is the layer that almost no AI coverage addresses — and where some of the most durable economic value is quietly accumulating.

Power: AI's Bill Is Becoming Everyone's Bill

AI does not run on ideas. It runs on electricity — enormous, continuous, and rapidly growing quantities of it.

Statistic | Data Point | Source |

|---|---|---|

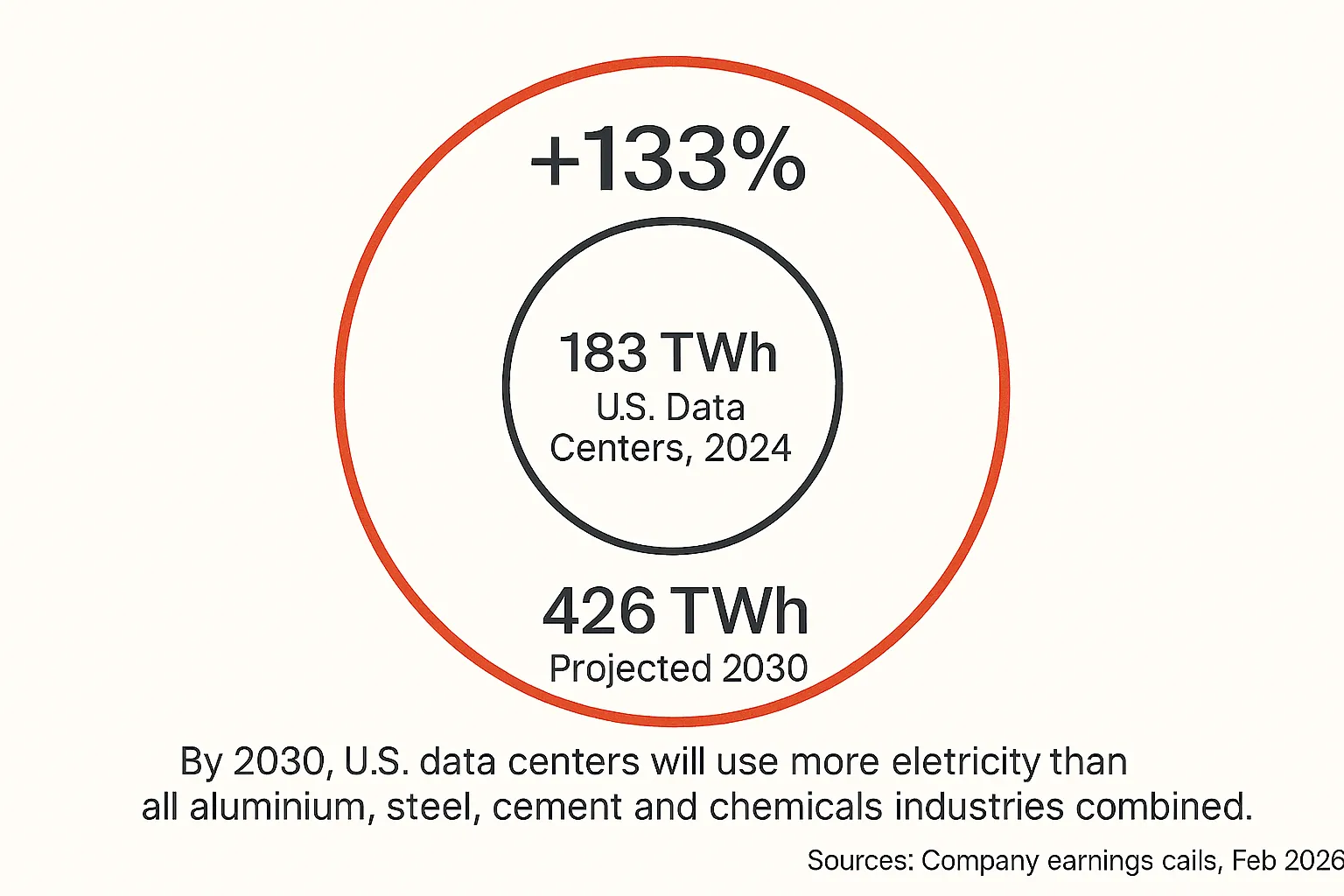

U.S. data center electricity consumption, 2024 | 183 TWh (4%+ of total U.S. electricity) | |

U.S. data center electricity projected, 2026 | 250+ TWh | |

U.S. data center electricity projected, 2030 | 426 TWh (+133% from 2024) | |

Global data center electricity projected by 2030 | 945 TWh (≈ Japan's entire annual demand) | |

U.S. data center share of all electricity demand growth to 2030 | ~50% | |

Global data center investment, 2024 | ~$500 billion (nearly double 2022 levels) | |

Electricity price increase near data center clusters since 2020 | Up to 267% | |

PJM market price increase attributed to data centers (2025–26) | $9.3 billion | |

Projected U.S. residential electricity bill increase from data centers by 2030 | 8% nationally; up to 25%+ in Virginia | |

U.S. electricity demand growth in 2025 | +2.3% (record growth post-years of flat demand) |

By 2030, the IEA projects U.S. data centers will consume more electricity than all of the country's aluminium, steel, cement, chemicals, and other energy-intensive industries combined. That demand must be sourced from somewhere — and the companies building power plants, gas turbines, transmission infrastructure, nuclear capacity, and cooling systems to meet it are quietly compounding returns that most investment analysis ignores.

By 2030, the IEA projects U.S. data centers will consume more electricity than all of the country's aluminium, steel, cement, chemicals, and other energy-intensive industries combined. That demand must be sourced from somewhere — and the companies building power plants, gas turbines, transmission infrastructure, nuclear capacity, and cooling systems to meet it are quietly compounding returns that most investment analysis ignores.

The infrastructure bottleneck has already shifted once, and it is shifting again. As one Fortune analyst described the evolution: first it was a GPU shortage, then a chip shortage, now it is a physical shell shortage — the actual buildings and power connections cannot be built fast enough to house the hardware already ordered.

The Data Center Pipeline Is Real

As of mid-2025, researchers tracking the pipeline had identified 294 data center projects totaling 73.6 GW of demand. Over 8.9 GW across 105 projects were targeting operation by end of 2026, with 47 already under construction — and no widespread cancellations had been recorded.

The geographic diversification is accelerating too, with major announcements in the UK, France, Japan, and India alongside the traditional U.S. hubs of Northern Virginia, Dallas, Chicago, and Phoenix.

⚡ Key Takeaway: If you want to find the durable long-term winners of the AI era — the modern equivalent of the railroad companies that outlasted every gold rush — look at energy infrastructure, data center construction, power equipment manufacturers, and cooling system providers. These are slower stories than Nvidia, but potentially more lasting ones. The bill for AI compute is eventually paid in kilowatt-hours, and someone has to supply them.

5. The Circular Flow Problem

Here is the structural risk that Deutsche Bank, Barclays, Mizuho, and a growing number of analysts raised explicitly in February 2026, following the hyperscaler capex announcements.

The majority of Nvidia's GPU revenue flows from the four hyperscalers. The hyperscalers buy GPUs, build data centers, and rent compute to AI companies like OpenAI and Anthropic. OpenAI and Anthropic use that compute to build models, which they sell back to enterprises — including, increasingly, to the hyperscalers themselves. Meanwhile, Nvidia has committed $100 billion to OpenAI, money that will cycle back to Nvidia in GPU purchases.

The result is a loop: hyperscalers fund model companies; model companies generate revenue that flows back to hyperscalers; hyperscalers use that revenue to buy more Nvidia chips. Nvidia sits at the center, collecting margin on every rotation.

The risk: if enterprise AI adoption stalls — if the 6% ROI problem documented in our statistics roundup does not resolve — the circular flow weakens. Every link in the chain is betting that enterprise monetization will scale fast enough to justify the infrastructure being built right now.

Analysts at Mizuho wrote in February 2026 that skeptical investors may view the potential doubling of capex as "leaving limited free cash flow in 2026 with uncertain return on investment." Barclays, Morgan Stanley, and Pivotal Research issued similar warnings in the same week.

The market voted with its feet: the four hyperscalers lost a combined ~$950 billion in market cap in the days following their earnings calls.

⚡ Key Takeaway: The AI economy currently has one indisputable winner (Nvidia), several plausible but expensive winners (AWS, Azure, Google Cloud), several historic-scale bets (OpenAI, Anthropic), and a set of quiet compounders (energy infrastructure, construction, broader semiconductors). The entire structure depends on enterprise AI ROI improving — which is the same story we started with.

6. What This Means for Business Leaders

If you are not Nvidia and you are not a hyperscaler, this data has three practical implications.

You are the market being sold to, not the one profiting. The infrastructure layer — GPU costs, cloud compute, software licensing, energy — extracts value from every AI investment you make. Understanding this does not mean you should not invest. It means you should be clear-eyed about where your money is going and demand proportional returns.

The ROI gap is not random. The 6% of organizations seeing real AI returns share a consistent pattern: they redesign workflows, invest 70% of their AI resources in people and process rather than tools, and treat AI as an operating model transformation rather than a technology purchase. They are not just buying more shovels — they are fundamentally changing how they mine.

The infrastructure winners are real and largely underreported. If you are evaluating AI investments from a portfolio or strategic partnership lens, the companies supplying power, cooling, chips, and cloud compute are the most financially defensible positions in the AI ecosystem right now. The model layer is a series of expensive, unproven bets. The shovel merchants — especially in energy — are already counting returns.

Summary: Who Is Actually Winning Right Now

Layer | Current Leaders | Financial Status (Feb 2026) |

|---|---|---|

AI chips | Nvidia | Profiting massively — $130B+ revenue, 73%+ margins, $65B quarter guided |

Cloud infrastructure | AWS, Azure, Google Cloud | Growing fast — but burning free cash flow to fund $650B in 2026 capex |

AI models | OpenAI, Anthropic | Revenue growing fast — but losses are larger and growing faster |

Energy & power infrastructure | Utilities, gas operators, nuclear | Quietly compounding — AI is a generational demand tailwind |

Enterprise AI adopters | Top 6% only | Strong returns; 94% still not capturing meaningful value |

Primary Sources & References

IG International — Nvidia Q4 FY2026 Earnings Preview (Feb 2026)

CNBC — Tech AI Spending Approaches $700 Billion in 2026 (Feb 2026)

Yahoo Finance — Big Tech Set to Spend $650 Billion in 2026 (Feb 2026)

Fortune — Big Tech's $630 Billion AI Spree Now Rivals Sweden's Economy (Feb 2026)

TechCrunch — Amazon and Google Are Winning the AI Capex Race — But What's the Prize? (Feb 2026)

Motley Fool — Nvidia Stock Investors Got Good News From the Hyperscalers (Feb 2026)

Fast Company — How Much Amazon, Microsoft, Meta and Google Are Spending on AI in 2026 (Feb 2026)

Campaign US — Big Tech's AI Spend in 2026: Following the Money (Feb 2026)

eWeek — Google, Microsoft, Meta, and Amazon Plan $650 Billion AI Spending Push in 2026

Silicon Republic — Big Tech's $650B Capital Expense Bill, 2026 (Feb 2026)

Fortune — OpenAI Cash Burn Rate, Annual Losses Through 2028 (Nov 2025)

eMarketer / Deutsche Bank — OpenAI Forecast $143B Cash Outflow (Dec 2025)

RD World Online — Facing $14B Losses in 2026, OpenAI Seeks $100B in Funding (Feb 2026)

WebProNews — OpenAI Revenue Triples to $20B in 2025 Amid $17B Burn (Jan 2026)

Pew Research Center — What We Know About Energy Use at U.S. Data Centers (Oct 2025)

Rigzone — USA Data Center Electricity Demand Projected to Triple (Nov 2025)

nZero — U.S. Power Demand Hits New Highs Driven by Data Centers and AI (Dec 2025)

Bloomberg — How AI Data Centers Are Sending Your Power Bill Soaring (Sep 2025)

Published by AI Shortcut Lab · Helping leaders harness AI without the hype.

Comments (0)

Leave a Comment